What is demand?

Demand is defined as want or willingness of consumers to buy goods and services.

In economics willingness to buy goods and services should be accompanied by the ability to buy (purchasing power) and is referred to as effective demand.

Law of demand

The law of demand is an economic law that states that

consumers buy more of a good when its price decreases and less when its price increases, ceteris paribus.

It states that when price increases, the amount demanded will fall and when prices fall, the amount demanded will rise.

Rationale of the law of demand

There are two reasons for a fall in demand when the prices increase.

Income effect: People feel poorer. As the price of a good rises the purchasing power of people to buy that good will fall. This is known as income effect.

Substitution effect: Some people might shift to cheaper alternatives/substitutes once the price of a good rise, thus leading to a fall in demand for that good.

Watch a Video

Factors affecting demand

Change in people’s income: More the people earn the more they will spend and thus the demand will rise. A fall in income will see a fall in demand.

Changes in population: An increase in population will result in a rise in demand and vice versa.

Change in fashion and taste: Commodities or which the fashion is out are less in demand as compared to commodities which are in fashion. In the same way, change in taste of people affects the demand of a commodity.

Changes in Income Tax: An increase in income tax will see a fall in demand as people will have less money left in their pockets to spend whereas a decrease in income tax will result in increase of demand for products and services because people now have more disposable income.

Change in prices of Substitute goods: Substitute goods or services are those which can replace the want of another good or service. For example margarine is a substitute for butter. Thus a rise in butter prices will see a rise in demand for margarine and vice versa.

Change in price of Complementary goods: Complementary goods or services are demanded along with other goods and services or jointly demanded with other goods or services. Demand for cars is affected the change in price of petrol. Same way, demand for DVD players will rise if the prices of DVDs’ fall.

Advertising: A successful advertising campaign may affect the demand for a product or service.

Climate: Changes in climate affects the demand for certain goods and services.

Interest rates: A fall in Interest rate will see a rise in demand for goods and services.

Watch a Video

What is Supply?

Supply refers to the amount of goods and services firms or producers are willing and able to sell in the market at a possible price, at a particular point of time.

Law of Supply

It states that when the price of a commodity rises, the supply for it also increases.

The higher the price for the good or service the more it will be supplied in the market. The reason behind it is that more and more suppliers will be interested in supplying those good or service whose prices are rising.

Factors affecting Supply

Price of the commodity: A rise in price will result in more of the commodity being supplied to the market and vice versa.

Prices of other commodities: For example if it is more profitable to produce LCD TVs then producers will produce more LCD TVs as compared to PLASMA TVs. Thus the supply curve for PLASMA TVs will shift inwards i.e. a fall in supply.

Change in cost of production: Increase in the cost of any factor of production may result in the decrease in supply as reduced profits might see producers less willing to produce that commodity.

Technological advancement: Improvement in technology results in lowering of cost of production and more profits for the producer and thus more supply of that commodity.

Climate: Climate and weather conditions affect the supply of commodities especially agricultural goods.

Equilibrium

Equilibrium is a point of balance or a point of rest. A more complex definition is

It is the point at which quantity demanded and quantity supplied is equal. Market equilibrium, for example, refers to a condition where a market price is established through competition such that the amount of goods or services sought by buyers is equal to the amount of goods or services produced by sellers. This price is often called the equilibrium price.Equilibrium is a state in market where economic forces are balanced and in the absence of external influences the (equilibrium) values of economic variables will not change.

In the graph below the point at which the demand curve meets the supply curve is the equilibrium price.

Equilibrium is ‘self righting’

It means that if we try to move away from the equilibrium situation it will revert back to its original position, if there is no external disturbance.

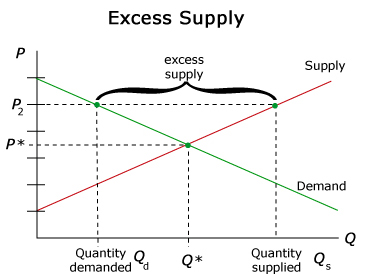

Figure below explains the concept.

In this diagram the equilibrium price is P* and the quantity supplied Qe. However, the prices have been increased to P2. As the price has increased it will lead to more suppliers entering the market and supply increasing to Qs. At the same time, a increase in price to P1 will lead to a fall in demand (as per the law of demand) i.e. Qd. This will create an excess supply situation. Now the suppliers will find it difficult to sell their goods and they will have to reduce their price to attract more consumers. This will go on till the price again reaches its initial level i.e. P*. Hence the situation is self righting if the prices are raised without any external reason.

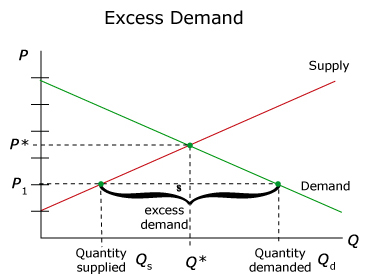

Similarly, in the figure below

we can see that the prices have been artificially reduced from P* to P1. This leads to a fall in supply from Q* to Qs (as per law of supply). As the prices fall from P* to P1, people can afford to buy more of that good and demand increase from Q* to Qd. Again an excess demand situation is created. In order to get the most out of this situation the suppliers will start increasing their price. On the other hand demand will start falling as the prices increase. This will all continue till the prices settle at equilibrium price i.e. Pe. Hence we can say that equilibrium is ‘self-righting’

Movement to a new equilibrium

The equilibrium price remains unchanged till the demand and supply curves retain their position. The moment there is a shift in any of the components, a new equilibrium will be formed.

Effect of change in Demand and Supply

Demand |

Supply |

Equilibrium price |

Equilibrium quantity |

|

Increase |

Unchanged |

Rise |

Rise |

|

Decrease |

Unchanged |

Fall |

Fall |

|

Unchanged |

Increase |

Rise |

Rise |

|

Unchanged |

Decrease |

Rise |

Fall |